What the US-Israel-Iran War Means for Your Portfolio, Your Country, and the World Economy

Your energy bill is about to tell you what the White House won’t. While governments manage the narrative and financial media debates whether oil at $80-$100 is a ‘buying opportunity,’ the war reshaping the global economy is already in motion. US and Israeli strikes on Iran triggered a cascade that is now hitting many countries simultaneously, choking the world’s most critical shipping lane, and quietly threatening everything from South Korean semiconductor factories to Indian wheat harvests. Whether this resolves in weeks or drags into months determines not just what happens to oil — it determines which portfolio scenario you need to be prepared for. Understanding the difference is worth real money.

This is what’s actually happening. And more importantly, this is what you do about it.

What stock markets are telling you

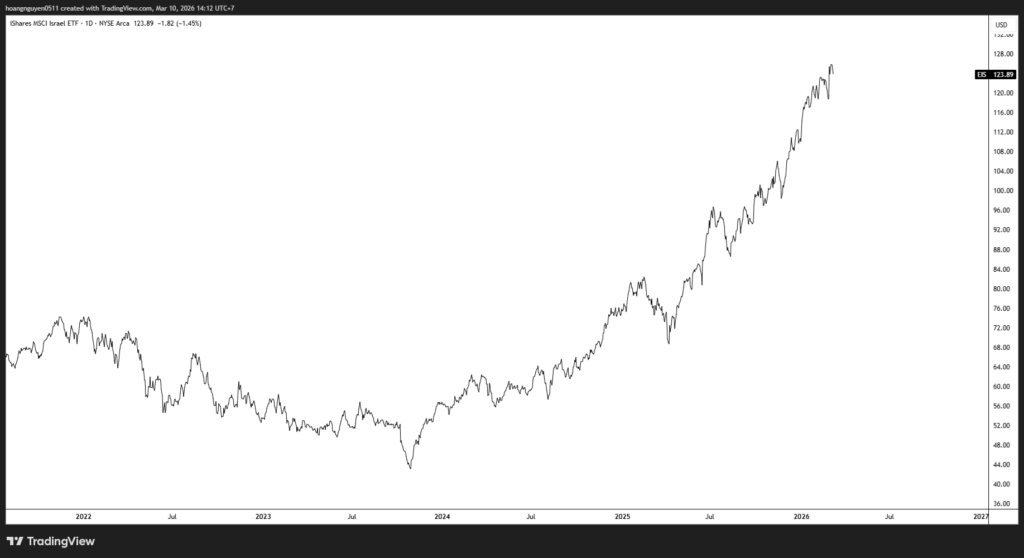

Let’s start with the signal that the panicians don’t want you to focus on: the Israeli stock market is at all-time highs.

Think about that for a moment. Israel — the country in the middle of this war, the one absorbing Iranian counterstrikes — is trading as if none of this is an existential crisis.

And it’s right.

The data backs the market’s calm. Iranian offensive capability has been severely degraded. The volume of munitions being launched has fallen sharply. The interception rate has risen precipitously. And crucially, Iran has shifted from missiles to drones — a downgrade in destructive capability, not an upgrade. A drone attack is noise. A ballistic missile is a different matter. Iran is running out of the latter.

There’s something else the Israeli market knows. In 2022, when Russia invaded Ukraine and energy prices spiked, the Israeli market fell — because Israel imports oil and the price hurts.

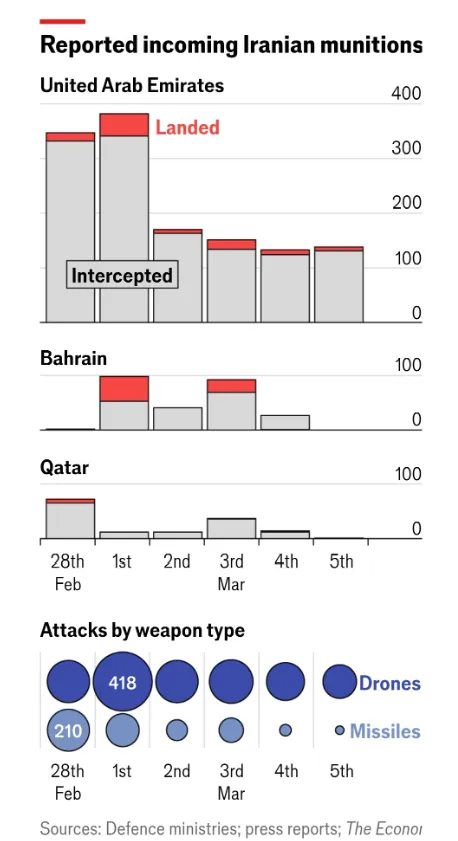

Today the market is up, not down. That divergence is telling you something real: the security situation is fundamentally better than it was. Iran’s military leadership was decapitated early in this conflict. The chain of command broke. Regional generals were given standing orders to inflict maximum economic damage on Gulf states — hitting Qatar, the UAE, Bahrain — and now operate largely independently. That’s important for reasons we’ll come to.

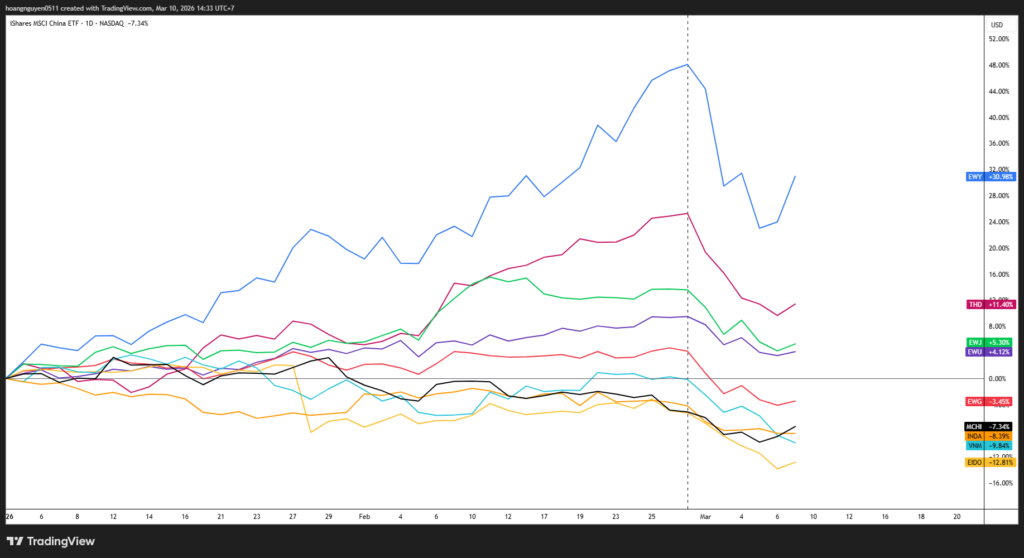

Looking at other stock markets globally, we can have a feel for which countries got hit by this war. European markets, Japan, Korea, China, India, Thailand, Indonesia, Vietnam just to name a few.

But let’s keep this opening part brief, I will resume the winners and losers later in this report.

So why is oil spiked up to +$100?

Because the war Israel is winning militarily is still causing economic chaos in the shipping lanes. And the question of how long that chaos persists is the question everything else depends on.

The most important question

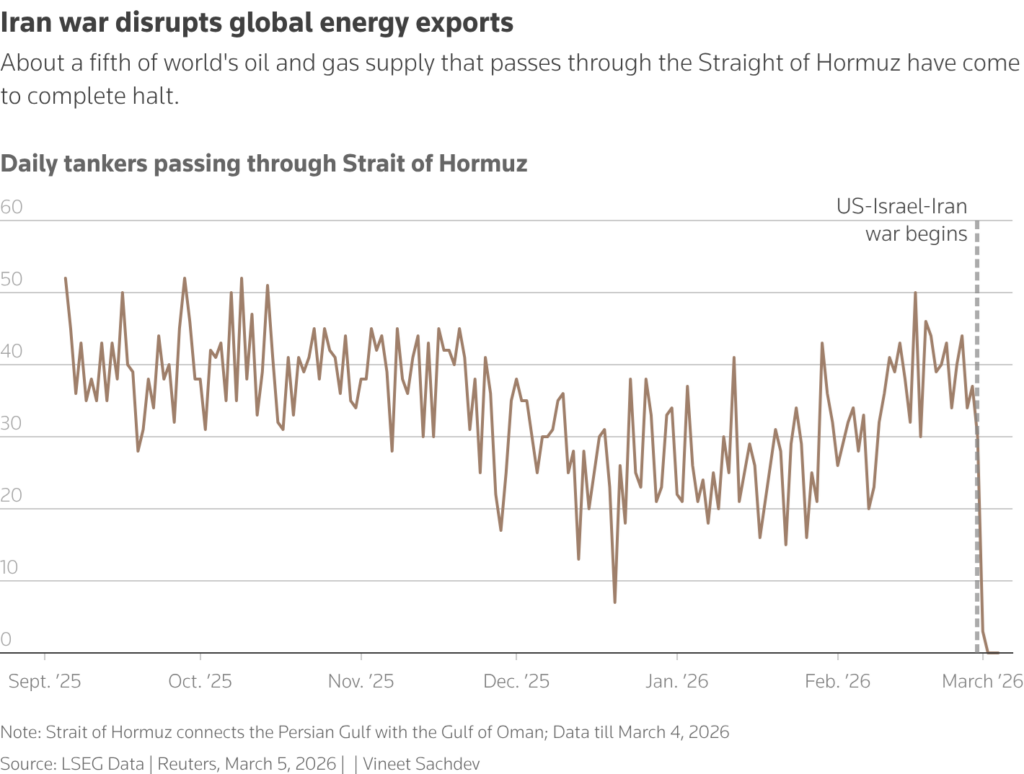

Twenty percent of global crude oil transits through the Strait of Hormuz. Roughly 90% of Persian Gulf oil flows to Asia. One disruption to that corridor and you’re not just repricing oil — you’re repricing the entire Asian economy.

So can Iran close it for as long as it wants? And do they really want to do it?

The first case is that: Iran can’t close the Strait for long — and the history of commodity disruptions proves it.

Consider the parallel with Russia and Ukraine. When Russia invaded, it effectively closed Ukrainian grain exports through the Black Sea. Russia had overwhelming regional military dominance. It threatened to target any ships carrying grain. And yet Ukraine was still able to export through the use of drone and missile strikes on Russian assets. Wheat spiked dramatically — then collapsed. The disruption was real, the price spike was real, but the closure was not permanent.

Now apply that logic to Hormuz. Iran faces a far more powerful adversary — the combined military capability of the US and Israel. If Russia couldn’t stop Ukrainian grain exports against a fraction of that firepower, why would you bet that Iran can close the world’s most strategically vital waterway indefinitely? And there’s a self-defeating dimension that compounds Iran’s problem: Iran earns everything through the Strait. Every barrel it prevents from transiting is a barrel of its own revenue that disappears. A regime that can’t pay its military, its bureaucrats, its population, doesn’t last long. Closing the Strait could be economic suicide for the country that most depends on it being open.

The second casse is that: It’s not actually Iran shutting down the Strait; it’s Western insurance firms.

Most of the Strait runs through Omani territorial waters — not Iranian. Iran doesn’t need to physically blockade it. It only needs to make Western underwriters nervous. And it has succeeded spectacularly at that.

Western insurance companies have canceled tanker policies or made premiums so prohibitively high that commercial shipping has effectively ground down. The disruption is legal and financial, not purely military. A single EU regulatory intervention could suspend the relevant insurance requirements and reopen the lane within 30 days. That call has not been made. The absence of that intervention is itself a policy signal. Maybe someone, somewhere, wants the disruption to continue for now.

Add one more dimension the optimists miss: the collapse of the Iranian regime is in nobody’s interest in the region. Not Pakistan. Not Turkey. Not India. Not Afghanistan. Not the Arab states who are publicly aligned against Tehran but privately terrified of what comes after it. A failed Iranian state means mass migration, militant spillover, and the permanent loss of Iranian oil supply from global markets — potentially for years. That’s a worse outcome than a managed, contained Iran. Which means the political pressure to end this conflict may be weaker than markets assume.

The honest answer: nobody knows how long this lasts. But I guess I should make a bet that this situation should not last long.

Winners and Losers

Let’s be direct about who is being hurt and who is benefiting. The geopolitical map here is radically different from what the Western media narrative implies.

China is not the biggest victim — despite what the headlines suggest. Between 2016 and early 2024, China’s total observed aboveground crude oil inventory has ranged from 850 million to a bit over 1 billion barrels. Total inventories were estimated at between 1.1 billion and 1.2 billion barrels – equivalent to around over three months of imports.

China imports Russian and Central Asian oil via overland pipeline routes that bypass the Strait entirely. It has the world’s highest electric vehicle penetration — not out of environmental enthusiasm, but as a national energy security strategy built precisely for moments like this one. And in the aftermath of the June war, China and Russia finalized a gas pipeline deal that had been dormant for years. China saw this coming. It is positioned accordingly.

The real victims are India, South Korea, Japan, Thailand, and the Philippines. The Korean KOSPI fell 12-15%. Japan’s Nikkei dropped 8%. These are the countries probably calling the White House in a panic — not China.

They are US allies being economically destroyed by a war their ally started.

India’s situation deserves particular attention — and particular bluntness. The US granted India a 30-day waiver to continue buying Russian crude. That waiver is not generous. It is a face-saving admission that the Strait disruption might be not ending quickly. India had never actually stopped buying Russian crude anyway — it was flowing through Oman via a shadow market. The waiver formalizes a reality Washington had been pretending didn’t exist. But the deeper question India should be asking itself is this: why does a country of 1.4 billion people, the world’s fifth largest economy, need permission from Washington to buy energy on the open market? That question will reshape Indian foreign policy for a generation.

The poorest nations face something potentially worse than COVID. Bangladesh, Pakistan, Vietnam, the Philippines, and multiple African nations are watching their currencies collapse against a dollar strengthened by flight-to-safety flows. They cannot afford oil at these prices. They cannot afford food at the prices that will come. When people cannot heat their homes or cook their food, they move. Every Western politician who rails about migration while supporting this conflict is helping cause the migration they claim to oppose.

The winners are Vladimir Putin and Donald Trump. Russia benefits directly from higher oil prices and, critically, from the collapse of Western ability to sustain pressure on Russian exports simultaneously. You cannot sanction Russia AND destabilize the Middle East at the same time. Europe understands this and is quietly resuming Russian energy purchases — a development that will receive exactly zero honest coverage in mainstream Western media.

There is a broader strategic logic here worth examining plainly. US national security strategy in 2025 explicitly states that American world dominance requires two things: AI supremacy and abundant cheap energy for the US, with expensive energy for competitors. Controlling the waterways is how you control the energy. The helium angle fits this framework precisely: disrupting Qatar’s helium supply cripples Asian semiconductor manufacturing, and the US is the replacement supplier. History offers a useful parallel. Britain and the Soviet Union jointly invaded Iran in the 1940s to prevent a German railway from providing a troop route to the Soviet border. China has now built a Belt and Road railway from Beijing to Tehran, with plans to extend it to southern Iraq’s oil fields — another corridor for accessing Middle Eastern energy without using the Strait.

These patterns may be not accidental.

Two scenarios come to mind

Here is where this article becomes more useful to you. It has direct implications for how you should be positioned. Understanding both scenarios and what signals to watch is worth more than any single prediction.

We, as money managers, are paid to adapt, not paid to forecast.

Scenario A: The Inflation Path

The disruption persists for weeks or months. Oil remains elevated. LNG, fertilizers, NGLs, and helium stay constrained. Structural inflation embeds into the global economy.

In this scenario, central banks around the world have to take action.

- The ECB:

The ECB will be the first to hike. They still have fresh, painful memories of being late to the party in 2022, and they aren’t looking to repeat that mistake. They’re currently at a neutral stance and the economy is at potential.

March is too early for a move, but April is a “live” meeting. If the shock lasts, one hike won’t be enough. We’re talking about a new hiking cycle.

- The Bank of England:

The BoE comes next. Their first move will be taking rate cuts off the table. They’re already in restrictive territory and the economy is under-performing, so they have a bit more breathing room than the Europeans.

I don’t see a hike before the summer, but a durable shock means they’ll have to tighten eventually.

- The Fed:

The Fed will be the last to hike. Unlike the others, the Fed has a dual mandate—they have to worry about “maximum employment” while the world is burning. This stagflationary shock is a nightmare for them: it pushes inflation up but hits jobs at the same time.

More importantly, the Fed is under massive political pressure to ease, not tighten. Plus, the US is a bit more insulated because our gas prices aren’t as tied to the Gulf mess. A hike before autumn is unlikely, but again, if the shock is persistent, they’ll eventually have to face the music.

In this scenario, Bond markets continue their structural bear market, because you cannot own a fixed income instrument yielding 4.7% when inflation is structurally embedded at higher rates. This is the slow grind scenario.

The evidence for this scenario: 30-year Japanese Government Bonds are trading at 3.4% — a level that indicates market participants believe inflation is structural and persistent. The Israeli stock market’s all-time highs are consistent with inflation, not deflation. Other stock markets are still trading healthy relative to what has been happening recently despite some selloffs. Central bank gold purchases — which accelerated massively after the West seized Russian reserves and every non-Western central bank asked itself whether it could trust US Treasuries in a crisis — are also consistent with an inflation regime.

Because these banks are moving at different speeds, the yield curves are going to look very different:

- EMU: Bear-Flattening. The ECB hikes the short end to stabilize long-term inflation expectations. This keeps the long end in check, but watch out for spreads between high-debt and low-debt countries—they’re going to widen from these low levels.

- US: Bear-Steepening. This is the big one. Because the Fed is going to drag its feet on hikes while inflation rips, long-term expectations and yields are going to move higher. The long end of the curve is where the pain will be.

- UK: The Parallel Shift. Since the BoE is stuck in the middle, their curve will likely just shift upward or show a limited steepening.

Scenario B: The GFC Path

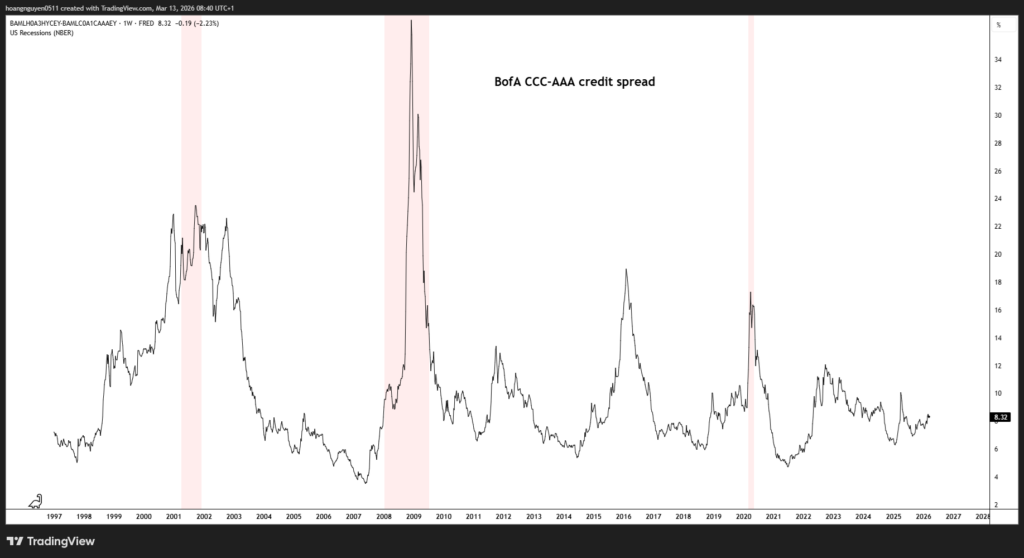

This is the scenario that deserves more serious treatment than it’s getting. Oil spiked from 2006 to 2008. That forced monetary tightening. Tightening caused credit markets to implode. Credit spreads blew out catastrophically. The result was not an inflation crisis — it was the Global Financial Crisis, the largest deflationary crash since the 1930s.

The concern is that the current oil spike recreates that exact sequence. Oil forces rates higher. Higher rates expose every over-leveraged institution in a financial system that has been running on near-zero rates for fifteen years. Credit spreads blow out. What starts as an energy disruption becomes a credit crisis. A deflationary crash follows.

The GFC wasn’t just driven by oil and rates. It was driven by an environment of inherently “deflationary” policies—the free movement of capital, goods, and labor, combined with government austerity. It was a world optimized for low prices.

Today, we have the opposite. We have a structural, bone-deep inflationary bias. Every policy lever the government has is being pulled in a stimulative direction.

Here is why this scenario is particularly dangerous: in every previous deflationary shock, government bonds provided safety. Investors fled to Treasuries. Yields fell. Bonds went up. The ‘long bonds, short equities’ playbook worked in 2008, in 2015, in 2020. But since COVID, government policy has been structurally oriented toward inflation. Governments are running fiscal deficits that are inflationary by design. In a GFC-style crash today, bonds might not rally the way they once did — because governments would respond with massive spending. The safe haven trade doesn’t work if the safe haven is itself an inflation casualty. That’s the real question embedded in the title: is it really different this time?

The answer is: possibly yes, and the implications are severe. The old playbook of ‘long bonds, short equities’ in a deflationary event may be broken. Which means there is currently no obvious safe harbor.

The key signal to watch: credit spreads. If this oil spike forces monetary tightening and credit spreads begin blowing out the way they did from 2006 to 2008, that is your early warning that we are on the GFC path, not the inflation path. Watch credit spreads.

If something is wrong

The S&P 500 is down only 4-5% from all-time highs. The market is pricing in what you might call the Venezuela scenario: a quick negotiated settlement, a short-term oil spike, a rapid return to normal. That assumption may prove correct. It may also prove catastrophically wrong.

Oil futures are telling the same optimistic story: spot prices have moved sharply higher, but prices further out the curve have barely moved. The market is betting this ends soon. If it doesn’t, the repricing along the whole curve will be violent and fast. But historically speaking, an extreme backwardation situation often marks the top in an oil move.

But the market is missing something even more important than the oil price itself. It is missing the sovereign wealth fund problem.

The Abu Dhabi Investment Authority, Mubadala, and the Qatar Investment Authority have been among the largest net buyers of Western equities and US Treasuries for decades. These funds have accumulated trillions of dollars in Western assets. They are, in a very real sense, part of what holds Western financial markets together from the demand side. Now consider what happens if this war drags on for months. Their domestic economies seize up. Food logistics become a genuine crisis. They need cash to fund domestic obligations — social stability programs, food subsidies, emergency infrastructure. They begin selling Western assets to raise that cash. They flip from net buyers to net sellers. That is a serious shock to both equity and bond markets simultaneously. This is one potential risk.

The flight-to-safety trade is also misfiring. The dollar is up — consistent with a risk-off move. But Treasuries are not seeing the large inflows that would normally accompany a flight to safety. Inflation fears and the safety bid are competing. This is not a normal geopolitical trade. The rules are different this time.

And the 60/40 portfolio — 60% equities, 40% bonds, the bedrock of institutional and retail asset allocation for four decades — is broken. Bonds no longer provide diversification from equity risk. This has been true since 2021. Every passing event makes it more true, not less. Owning long-duration government bonds at current yields in a structurally inflationary world is not safe. It is a slow, guaranteed loss of purchasing power.

So what to do?

Here is the synthesis. Not a prediction — a framework. What traders, investors, or money managers should think about:

First: stop panic selling. If you were smart enough to buy equities on Pearl Harbor Day—December 7, 1941—you massively outperformed the “wait-and-see” crowd who sat on their hands until the war ended. Geopolitical headlines are almost always a garbage reason to dump your long-term portfolio. Fear isn’t a signal to run; it’s a pricing mechanism. Use it. At OrigoX Research, we haven’t scaled down a single trade since we started last September. We’re still long Emerging Market equities, the energy sector, high dividend value stocks, and gold. We took profit on the oil futures trade, but the rest? We’re holding the line.

Second: inflation is the only story that matters. It is the structural backdrop of our lives now. Look at the tape: the Israeli stock market is at all-time highs, the S&P 500 won’t stay down, and central banks are hoovering up gold. Inflation isn’t necessarily a death sentence for stocks—in fact, it can be a tailwind for nominal returns. But for bonds at these yields? It’s a total dirtnap.

Third: your bond allocation is a disaster. Whether you’re an inflation hawk or just a skeptic, you end up at the same place. Holding a long-duration government paper at 4.7% in a world on fire makes zero sense. The 60/40 portfolio isn’t just “underperforming”—it is structurally broken. Maybe inflation protected bonds, but it’s not my taste.

Fourth: fix your framework. Something like 60% equities, 30% energy, and 10% gold has been the winning ticket for five years straight. The thesis doesn’t get weaker when a missile flies; it gets stronger. This isn’t some radical reallocation. The world has changed. Maybe it’s time to stop hugging US equities so tight and diversify into the rest of the map.

Fifth: gold is a serious asset again. And no, not for the reasons the gold bugs have been screaming about for twenty years. This is about the plumbing. The day the West seized Russian reserves, every non-Western central bank realized their Treasury holdings were a “maybe” in a crisis. The East—the Chinese, Japanese, Indian, and Korean retail investors—already gets this. They’re the ones buying. Western institutions haven’t even shown up to the party yet. When US short rates finally fall, the wave begins. Gold goes higher.

Sixth: AI and software companies aren’t going to zero. This selloff is a mix of “disruption anxiety” and geopolitical jitters, layered on top of a big concentration unwind. These companies are building the actual infrastructure of the global economy for the next two decades. If you went into a coma today and woke up in 2035, you’d want to own the AI hyperscalers. Fear is just letting you buy them cheaper than you could three months ago.

Seventh: you have to take a hard look at China. They have the cheapest capital, the cheapest electricity, and the cheapest manufacturing labor among the major players. The valuations are almost a joke. Plus, nobody in the West owns it, which means there’s no crowded trade to puke all over you. Compare that to the US: we’re 22% of global GDP but 70% of the index. Everyone is balls-deep in US tech. That is a risk, not a comfort. Fundamentals, momentum, valuation, and positioning are all pointing the same direction in China. That almost never happens at the same time.

Eighth: watch credit spreads. This is the “terrordome” signal. If the oil spike forces the Fed to tighten and credit spreads start widening like they did in 2007, that is your early warning that we are on the GFC path, not the inflation path. If that happens, the playbook changes instantly. The old instinct to hide in bonds might not save you this time because the safe haven itself is an inflation casualty. You have to be watching the screen before you’re forced to react. Watch credit spreads.

The Long View

The 1970s OPEC shock demonstrated the decisive power of Middle Eastern energy producers. It reshaped global politics, broke the Bretton Woods system, and forced the world to confront its dependence on a small group of states sitting on a geological accident.

The 2020s shocks may prove the exact opposite.

Every disruption of Middle Eastern energy supply accelerates the buildout of alternatives. Non-carbon energy. Non-Middle Eastern pipelines. Battery storage. Vehicle electrification. On-shoring in the US. Every time Iran or its proxies close a shipping lane, they make it more economically rational to build a world that doesn’t need that shipping lane. The strategic bargaining power they believe they are demonstrating is, on a long enough time horizon, the power they are destroying.

Iran may be making the same mistake OPEC made in the 1970s. The OPEC shock felt like the ultimate proof of leverage. It triggered an energy transition that took fifty years but has now advanced to the point where China’s electric vehicle penetration is rewriting the global oil demand curve in real time. Every oil shock shortens the timeline of that transition. Every closed shipping lane accelerates the geopolitical case for alternatives.

The war will end. The insurance problem will resolve, one way or another. The oil price will eventually adjust. But the structural shifts this conflict is accelerating — toward non-Western energy, toward alternative supply chains, toward gold over Treasuries, toward AI infrastructure over physical commodity dependence — those are not temporary. They are the lasting investment theme of this decade.

The question is whether your portfolio reflects the world as it is, or the world as it was five years ago.

The gap between those two answers has gotten significantly more expensive the last couple of weeks. OrigoX Research trades one to two themes at a time but we always look further into the future.