It’s this time of year again. Time for the annual tradition where I (and my AI 🤷) sift through thousands of pages of sell-side reports so you don’t have to.

I’ve read the “Year Ahead” outlooks from the respectable shops – the ones with the mahogany desks and the fancy models that drain your energy and leave you with zero original thoughts.

This report is my mental exercise to force myself to think about the stuff no one else is talking about – the surprise scenarios that actually make you money. This ritual served me well in the volatility of the last few years, and especially in 2025, when everyone was betting on “tariffs make USD stronger” and I shorted the dollar in early January while the herd got trampled.

The consensus right now is “Agreeably Unremarkable”. They think 2026 is going to be an extrapolated copy of 2025: steady growth, a gentle drift in inflation, and central banks slowly finding their “neutral rate” happy place. It’s a total snooze-fest. They’ve all crowded into the “K-shaped economy” narrative, saying that the heat at the top stays balanced by the cold at the bottom.

I’m not going to waste your time with word salad. I’m going to give you the 15-minute version of what I think is going to happen so you can get back to having fun with friends and family.

We are looking at a year of reacceleration and the return of inflation. It’s going to be bullish until it’s not.

Without further ado, in this report I will take you through:

- Quick review of 2025 and why US policy surprises didn’t have massive negative impacts.

- Consensus forecast of 2026

- Downside scenario

- Upside scenario

Get ready for the reflation trade and the supply wall that’s going to break it.

2025: why didn’t Trump policies have bigger negative impacts?

The 2025 post-mortem is in, and it’s a story of “wrong for the right reasons”. Twelve months ago, the bears were screaming over a potential US policy disaster. The fear? That a brutal combination of universal tariffs and strict immigration controls would trigger an immediate income squeeze and an inflationary spike that would break the back of the consumer.

While the “Liberation Day” policy shift was indeed more ideological and aggressive than the sell-side predicted, the catastrophic economic collapse never materialized. US GDP is tracking at 1.9%, only a hair below the 2.1% forecast from a year ago.

Why did the economy absorb the blow?

1. The Productivity Pivot (The “Efficiency” Hedge)

The most common question of 2025 was: If companies are paying billions in tariffs, why haven’t profit margins cratered?.

The answer is efficiency. After years of pandemic-era “labor hoarding” and acute staff shortages, corporate America was sitting on a degree of “buffer”. When the tariff regime hit, the focus shifted instantly from recruitment to productivity.

Firms successfully forced efficiency gains on their workforces to offset the margin squeeze. They didn’t pass the full cost to the consumer because they didn’t have to – they found the savings internally.

2. The Inventory Buffer

The second reason for the muted impact was simple preparation. The corporate sector wasn’t caught sleeping; they spent the tail end of 2024 and Q1 of 2025 building significant inventories in anticipation of “Liberation Day”. This effectively delayed the tariff-induced price hikes, giving the economy a multi-month runway to adjust.

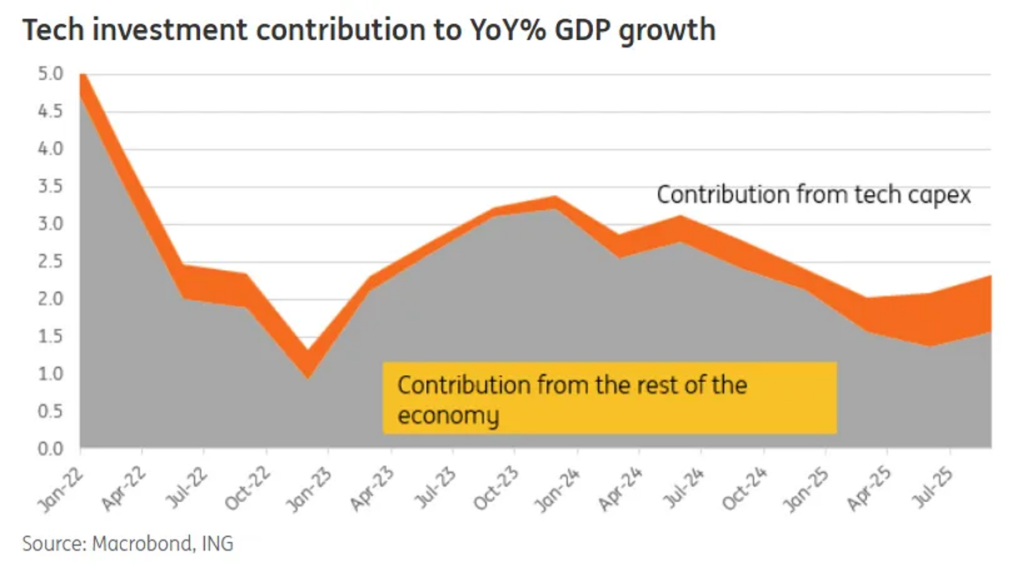

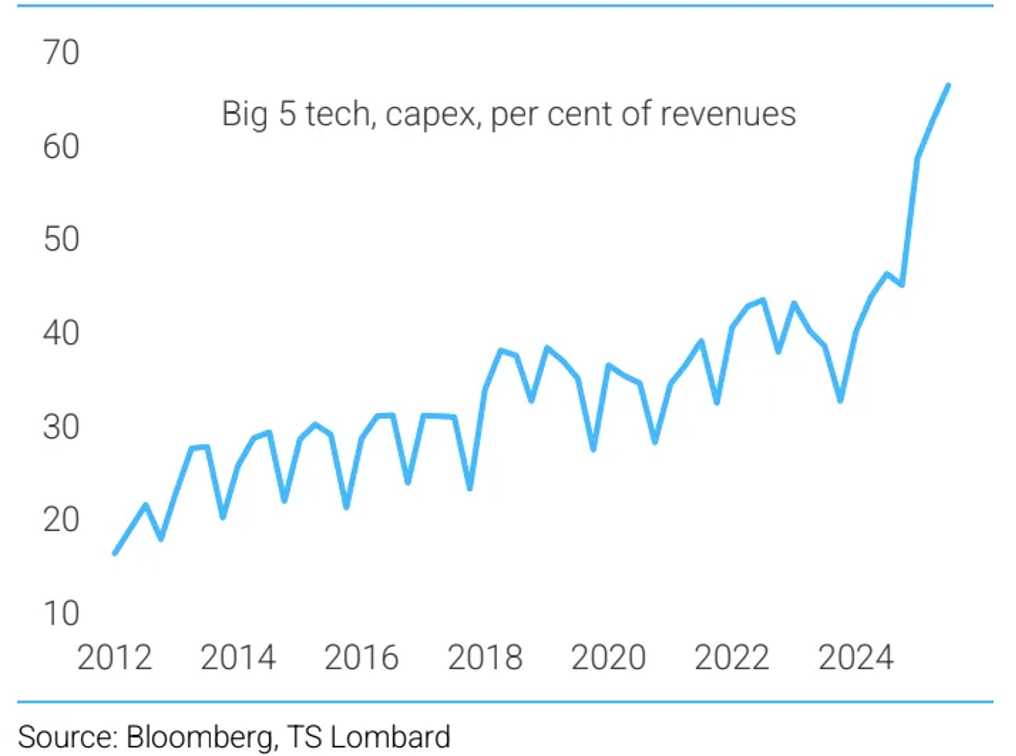

3. AI Capex

While some narratives suggest AI spending is the only thing keeping the U.S. economy afloat, the reality is more nuanced; AI capex has certainly surged, with Big 5 tech spending as a percentage of revenue hitting record highs in 2025. Big Tech’s capex binge cushioned the economy in 2025, propping up the top of the K while the bottom struggled.

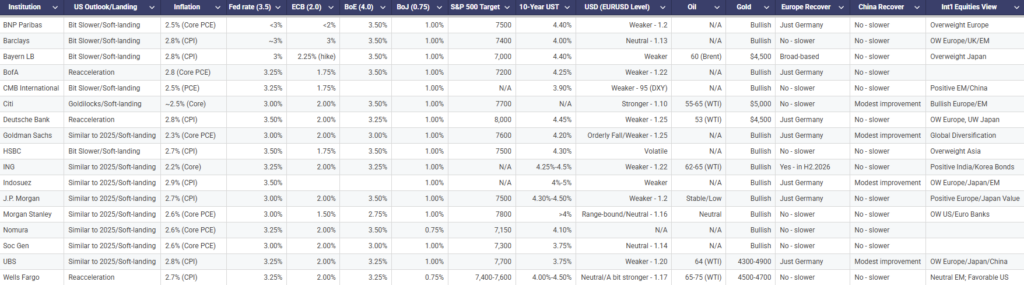

2026 Consensus: Agreeably Unremarkable

The current sellside consensus is a masterpiece of collective lack of imagination. Having been traumatized by three years of failed recession calls – the 2022 yield curve inversion, the 2023 rate hike fears and banking collapse, and the 2024 Sahm Rule trigger – economists are now too embarrassed to use the “R-word”. Instead, they have huddled together in the safety of the “Agreeably Unremarkable” forecast.

The Vanilla Projections:

- US Growth: Expected to flatline at a steady 2%.

- Inflation: A slow, painless drift lower toward 2.5%.

- Monetary Policy: A gentle glide path toward a neutral Fed rate of roughly 3.25%.

- The S&P 500: Most banks, from Goldman to JPM, are clustered around a target of 7500–7600, predicting another year of modest, “comfortable” returns.

- Europe and Japan show negligible improvement.

- China continues its structural fade.

This “Agreeably Unremarkable” outlook relies entirely on the K-Shaped Economy theory. The logic is simple: the weakness at the “bottom of the K” (struggling SMEs and low-income households) acts as a cooling agent for the heat at the “top of the K” (Big Tech AI capex and high-income spending). This creates a perpetual “Goldilocks” state – not too hot to revive inflation, not too cold to trigger a crash. It is a beautiful theory that I think is wrong.

THE BEAR CASE

For the past three years, calling for a U.S. recession has been the “house special” on the menu for Wall Street analysts and perma-bears alike.

- In 2022: Everyone was hyperventilating over yield curve inversion.

- In 2023: The panic shifted to rapid rate hikes choking the life out of the economy.

- In 2024: The spotlight turned to the labor market and the “Sahm Rule”.

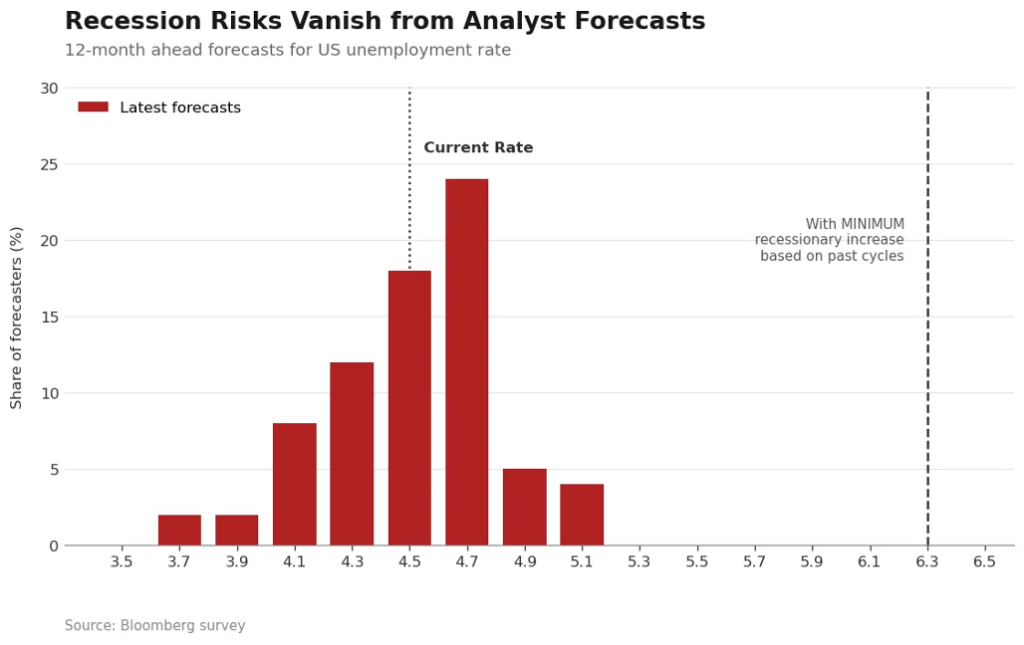

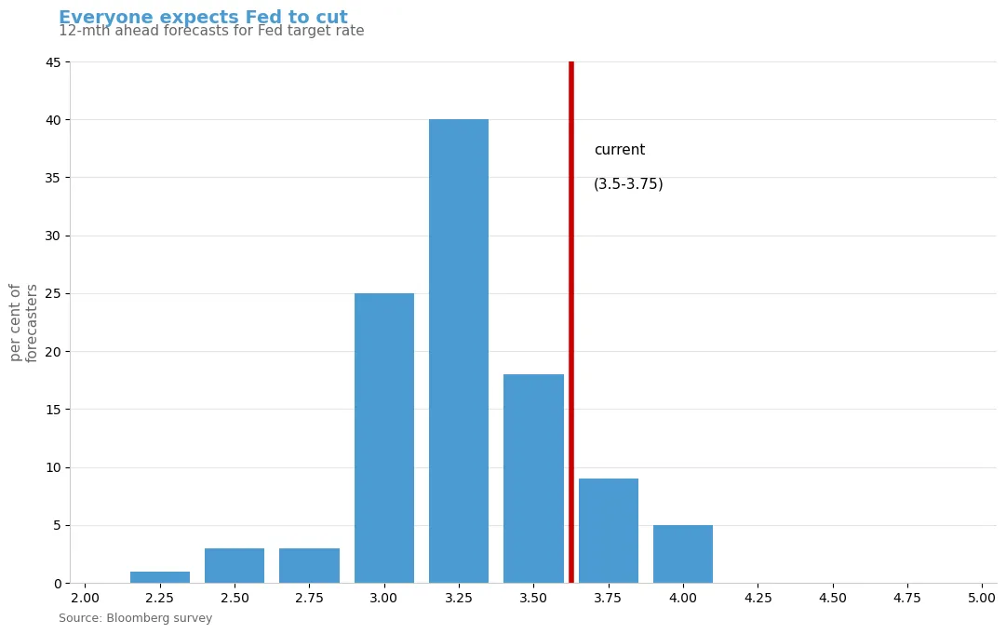

After getting it wrong so many times (the 2023 outlook was particularly embarrassing), economists have officially lost their nerve. They’ve stopped believing a recession is even possible. Look at the Bloomberg survey of unemployment forecasts: you’ll see a herd mentality where virtually nobody dares to predict a rise in the jobless rate of more than 40bps.

Historically, there has never been a U.S. recession where unemployment rose by less than 2%. The fact that every “expert” is now dodging this scenario makes me nervous. It feels exactly like the end of 2022, but in reverse. There’s a classic irony in macro trading: the recession usually hits the moment the last bear throws in the towel.

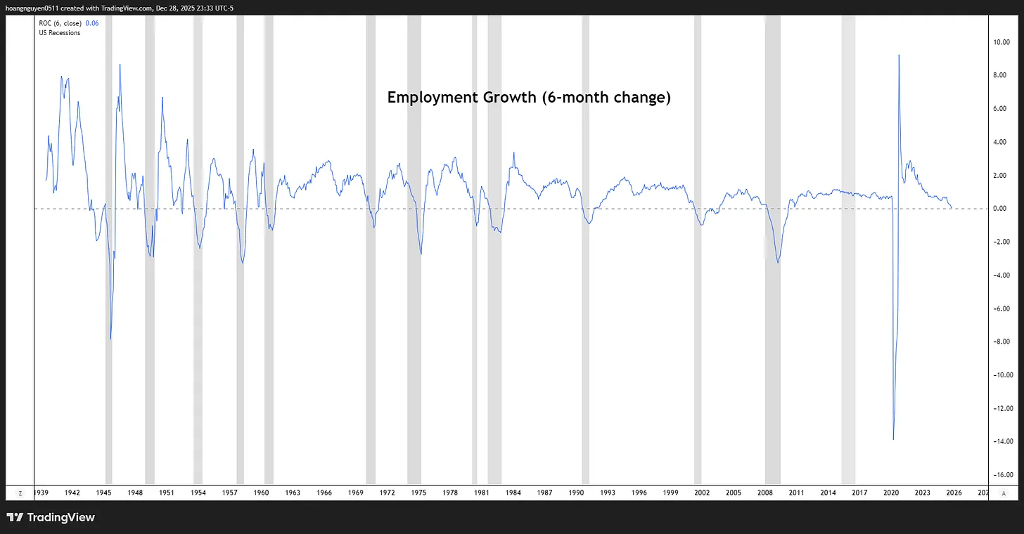

Superstition aside, the U.S. labor market is flashing some genuine yellow lights. The six-month change in payrolls is currently trending toward zero and very close to be negative – a move that has almost never happened outside of a recession. Usually, when this metric dips below the zero line, a plunge follows. Once the labor market actually cracks, it triggers a toxic feedback loop: weaker spending → falling profits → more layoffs.

However, I’m not convinced we’re falling off a cliff just yet. There are four reasons why this cycle might still have legs:

- The “Tariff Thaw”: A big chunk of the current hiring slowdown is driven by tariff uncertainty. That fog should lift by 2026.

- Shrinking Supply: The labor force isn’t growing like it used to. This means even modest job gains are enough to keep unemployment steady.

- No Structural Rot: There’s no deep macro-financial imbalance here. Tariffs are squeezing margins, sure, but the underlying plumbing of the U.S. economy isn’t broken.

- Efficiency Gains: As I’ve mentioned, firms are offsetting tariff pain by squeezing more productivity out of their existing staff. Corporate margins are still healthy by pre-COVID standards.

The Tail Wags the Dog: AI and “Credit Cockroaches”

“The stock market is not the economy,” the bulls say. True, but sometimes the tail wags the dog. If financial markets collapse, the real economy rarely stays upright. Analysts are currently fixated on two potential triggers:

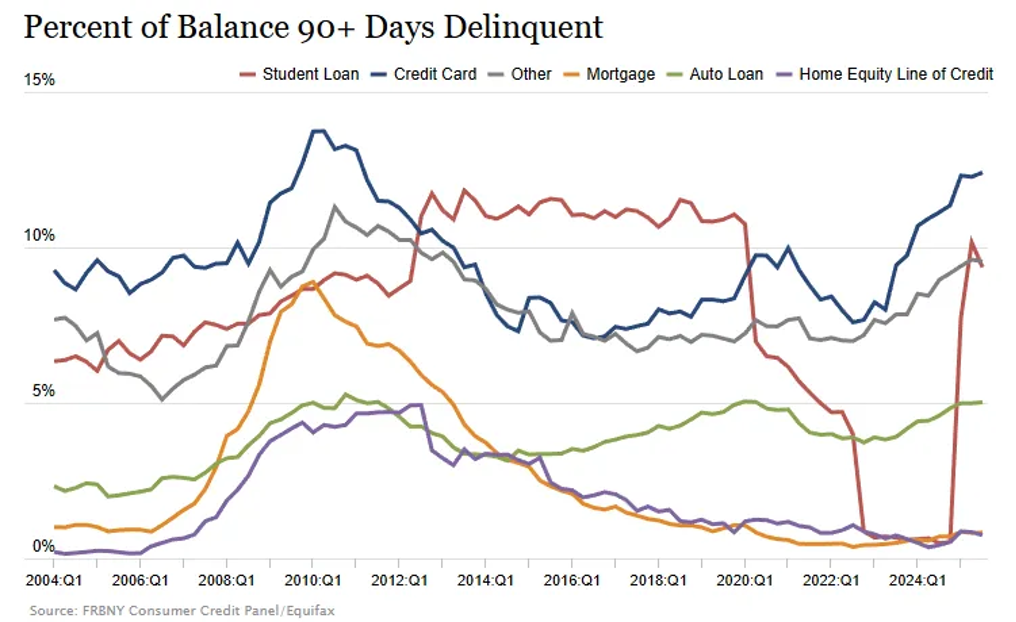

A) The Credit Market Jamie Dimon’s “credit cockroaches” comment caused a stir last summer. He was referring to the subprime auto lender Tricolor Holdings filing for bankruptcy. JP Morgan took a $180M charge-off, and Dimon’s point was simple: if you see one cockroach, surely there are others.

- Default rates are indeed rising in subprime auto, student debt, and parts of the mortgage market.

- Regional banks exposed to commercial property are hurting.

- Even private credit – the post-GFC darling – is seeing a wave of pessimism.

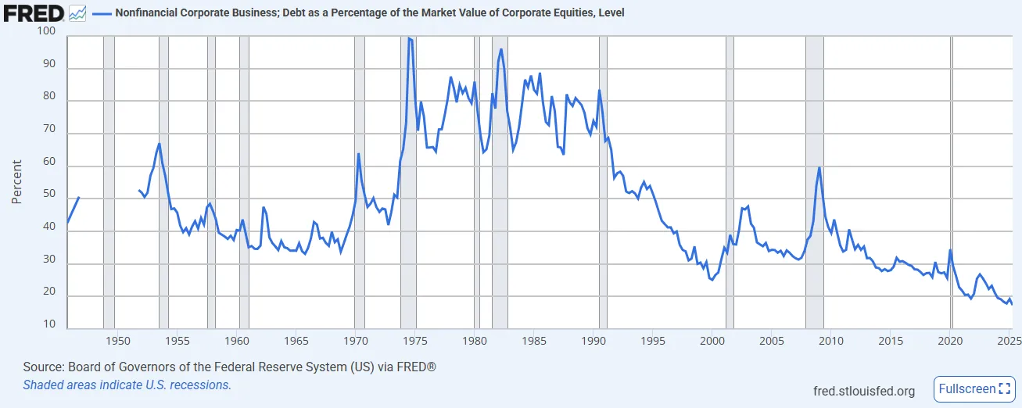

But honestly? The “cockroach” story feels overdone. While there are idiosyncratic messes, there is nothing that looks systemic. Financial leverage is lower than in past cycles, and we aren’t seeing a “credit event” on the horizon. If trouble comes, it will start in the economy, not the banks.

B) The AI Bubble Burst This is the more likely path to a market-led downturn. I don’t buy the argument that AI capex is the only thing keeping the U.S. out of recession , but the stock market is absolutely addicted to it. If NVIDIA gets hit in 2026, the ripple effect will be unavoidable. Falling prices crush confidence and freeze hiring.

What pops the bubble? Maybe data center returns continue to disappoint, or investors simply get tired of funding massive capex projects that bleed Big Tech’s balance sheets. I’m an AI skeptic at this time, but with the current momentum, this feels more like a 2027 problem than a 2026 one, especially since asset bubbles usually die when the central bank pivots.

If recession comes, will things turn bad?

In the short term, U.S. macro risks are skewed to the downside. The consensus is likely underestimating how weak the labor market looks right now.

But even if things look dicey in early 2026, a total collapse is hard to imagine. Private balance sheets are clean, there’s no massive leverage in the system, and policymakers will react with extreme force if cracks emerge. Between the U.S. fiscal impulse turning reflationary and global support from the rest of the world, the big theme for 2026 isn’t going to be recession – it’s going to be reacceleration . The only question left is the one that’s hardest to answer: Timing.

THE BULL CASE: Reacceleration and reflation

While the rest of Wall Street is busy falling asleep at their desks dreaming of a dull 2026, I’m looking at the data and seeing a global economy ready to pop a wheelie. The IMF and OECD think we’re stuck in a 3% growth loop forever.

I don’t buy it.

The consensus is positioned for a plateau, but I’m betting on the return of the other R-word: Reacceleration & Reflation (or Inflation if you want). Here’s why the “bounce” is going to be way bigger than the suits expect:

1. The “Wait-and-See” disappears

For the past year, the U.S. has been paralyzed by “Truth Social” policy chaos. Companies have been sitting on their hands, delaying hiring and capex because they didn’t know which way the tariff wind was blowing.

My bet? In 2026, the uncertainty fades. Even if the tariffs stay, the shock of them is gone. The bottom of the “K-shaped” economy is about to catch a major bid as labor demand returns. A tight labor market is the ultimate inequality-killer, and it’s coming back.

I think economists have a term for this. They call this Pent-up demand.

2. Trump’s Fiscal “Double-Tap”

The street is currently looking at Trump’s 2026 fiscal plan and seeing a big fat zero. The narrative is that the policies “cancel each other out” – a 1% GDP drag from tariffs perfectly neutralized by a 1% boost from the Big Beautiful Budget Bill. It looks like a wash on paper, but I’m more of a rate of change trader than an absolute level trader so I think they’re missing the shift.

The negative impact of the tariffs isn’t a future threat – it’s already in the rear-view mirror. U.S. companies have already coughed up roughly $250 billion in government revenue, acting as a massive tax on corporate earnings throughout 2025. But as we move into 2026, that growth-drag starts to fade even if the tariffs stay put.

Meanwhile, the “Beautiful” part of the budget hasn’t even started yet. The boost from tax cuts—including retroactive rebates—only begins to hit the tape in 2026. When you net out a drag that’s ending against a boost that’s just beginning, you aren’t looking at a “wash.” You’re looking at a 2% of GDP swing in the fiscal impulse.

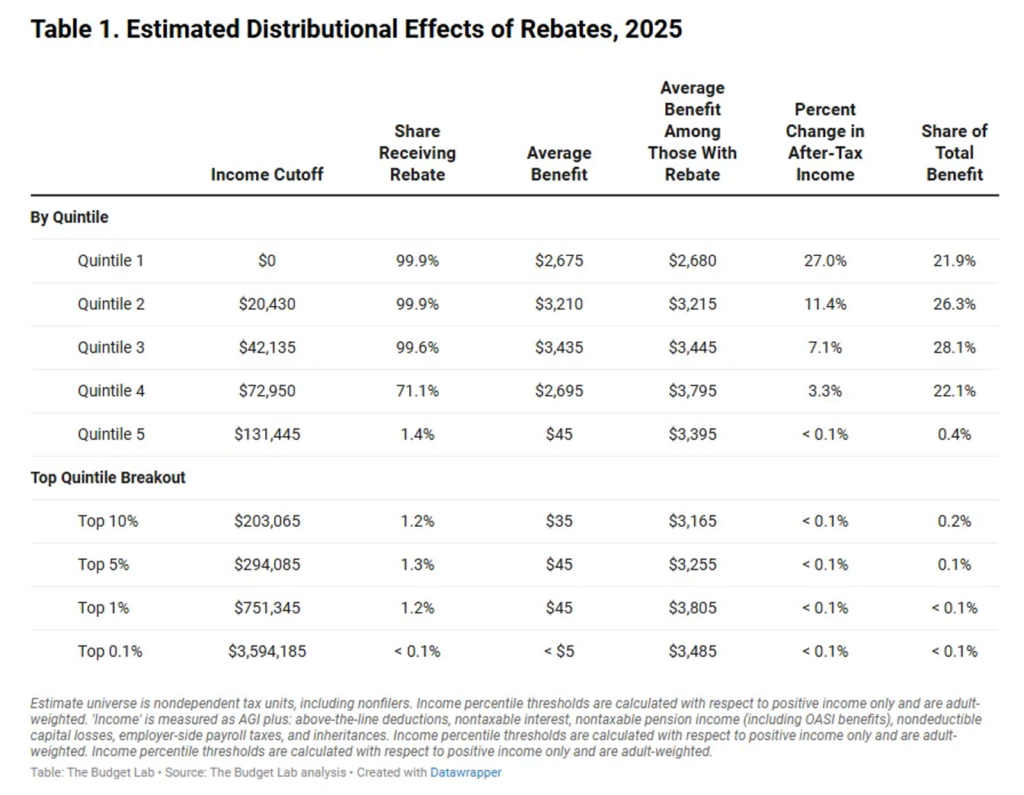

Because the “K-shaped” economy remains a significant political challenge, the administration is likely to pivot toward more direct support for lower- and middle-income households. This includes proposed tariff rebates of up to $2,000 per taxpayer for those earning under $200k.

- Significant Scale: This package could cost an additional 1% to 1.5% of GDP (per Budget Lab)

- High Marginal Propensity to Consume: Unlike broad corporate tax cuts, these rebates are laser-focused on the “bottom of the K,” where funds are more likely to be spent immediately rather than saved.

- Economic Reacceleration: While congressional approval remains a variable, the trajectory is clear: U.S. fiscal policy is turning decisively reflationary heading into 2026.

Markets price trajectories, not bills.

While the dull consensus expects 2026 to be a repeat of 2025, the data points toward a substantial fiscal reacceleration. We are moving from a period where companies were preparing for the “tariff hit” to a period where they – and the consumer – are preparing for a boost. This sets the stage for a stronger-than-expected rebound in activity, though it simultaneously heightens the risk of renewed inflationary pressure later in the year.

3. The Global “Laggard” Lift

While everyone is obsessing over the Fed, they’ve missed the fact that the rest of the world has been cutting rates for over a year. Debt costs are falling, credit is flowing, and rate-sensitive sectors like housing and big-ticket “durables” are waking up. When the Fed and BoE finally stop dragging their feet and hit “neutral,” the global economy gets a synchronized tailwind.

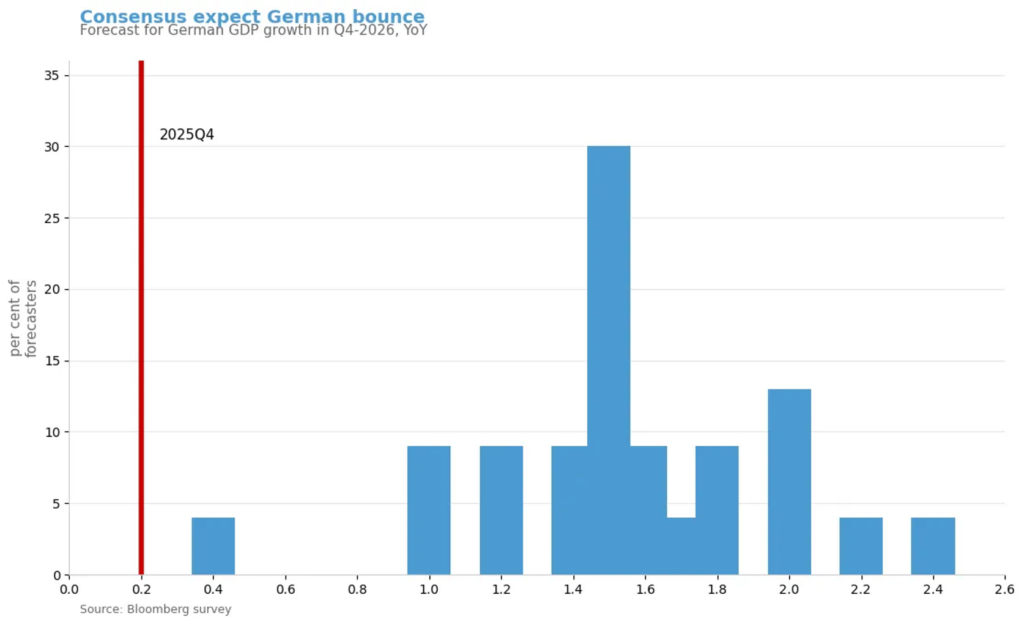

4. The German “Multiplier” Surprise

The consensus currently expects German GDP growth to accelerate from a stagnant 0.3% to roughly 1.5% by late 2026. This forecast assumes a standard fiscal multiplier of 1, based on an expected budget deficit widening of 0.8% of GDP. However, the actual impact could be significantly stronger for several reasons:

- Depressed Starting Point: Multipliers are typically larger in weak economies where there is no immediate threat of monetary tightening to offset the stimulus.

- Eurozone Spillovers: Germany is the primary export partner for most of Europe. A genuine revival in German domestic demand would likely pull the rest of the Eurozone out of its current slump—a factor the market seems to be underestimating.

5. China’s Cyclical Comeback

While the consensus has largely given up on Chinese stimulus due to deep structural issues – like the private debt overhang and the property market slump – they may be missing a cyclical opportunity.

- Policy Will: There is a clear intent from Chinese authorities to revive consumption and rebalance the economy.

- Learning from 2025: The modest stimulus measures of 2025 were withdrawn too early. In 2026, I think we can expect a more concerted effort to turn the economy around. Given how low expectations currently are, even a moderate positive surprise could shift the global growth narrative.

The Risk of Reacceleration: A Supply-Side Collision

A global reacceleration is usually great for risk assets, fueling the “reflation trade”. But in 2026, this demand will collide with a constrained supply side, particularly in the U.S. labor market.

The 3% GDP Scenario

Consider a scenario where U.S. demand recovers and GDP jumps to 3% – a full 100bps above consensus.

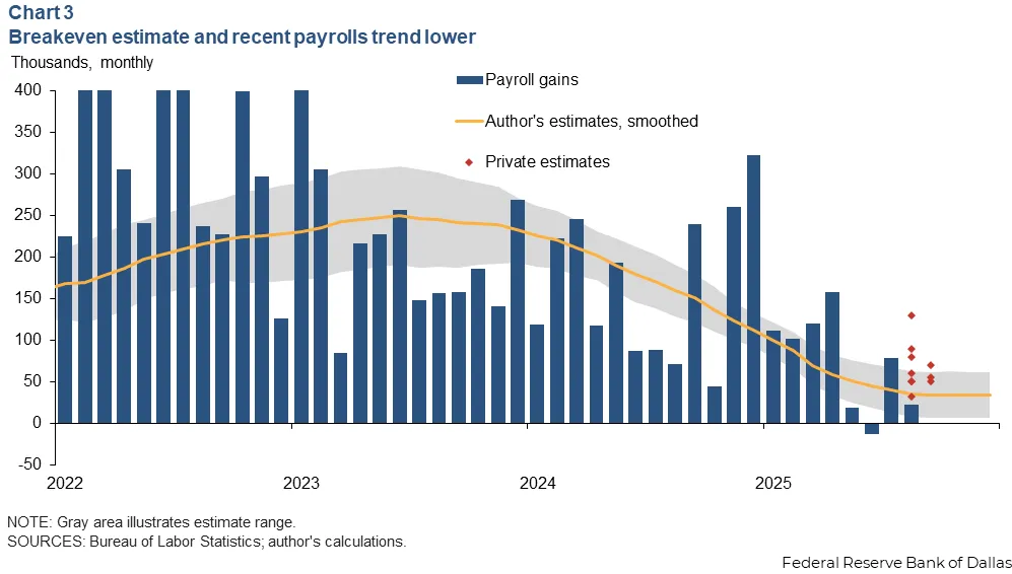

- Labor Demand: Ordinarily, this would require roughly 145k new jobs per month.

- Supply Constraint: However, the U.S. “breakeven” employment rate is estimated at only 35k per month due to tighter immigration controls.

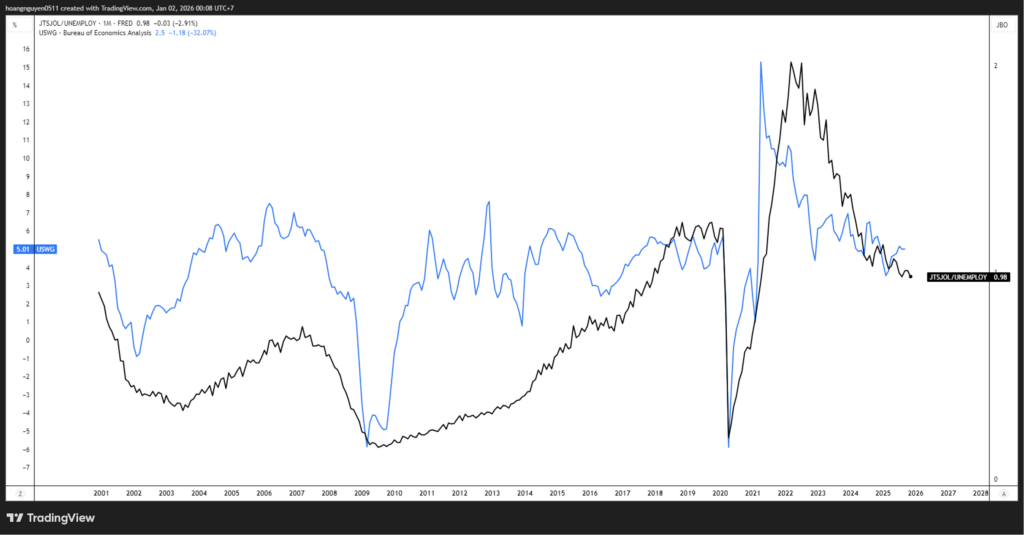

Starting from full employment, this gap would trigger acute worker shortages similar to the post-COVID era. This would drive the V/U ratio (vacancies per unemployed worker) sharply higher, serving as a leading indicator for aggressive wage growth.

The Return of Inflation

While the link between the job-vacancy-to-unemployment (V/U) ratio and wage growth is historically compelling, it is important to note that a tight labor market doesn’t always trigger an immediate inflation explosion. Inflation often lags behind the broader economic cycle, and continued productivity growth could theoretically keep unit labor costs in check for a while.

However, the data suggests several reasons for caution as we head into late 2026:

- Productivity Limits: Corporations have already pushed efficiency gains to offset 2025 tariff costs, but there are physical and operational limits to how far this process can run.

- The “Recovery Excuse”: After absorbing roughly two-thirds of tariff costs in 2025, firms may view a 2026 economic rebound as the perfect excuse to finally pass remaining costs to consumers. If this happens, inflation could return much faster than traditional Phillips-curve models suggest.

- The Monetary Debate: A reaccelerating economy and a tightening labor market are not what you expect to see if interest rates are truly “restrictive” or even “neutral”. This will spark a major debate over whether current rates are actually appropriate for the cycle.

- Policy Credibility: While we can’t observe the equilibrium rate (r*) in real time, the labor market acts as a clear signal for policy appropriateness. If the Federal Reserve remains unresponsive – or if a new leadership leans toward pushing rates lower regardless of the data – investors may begin to question the central bank’s independence, leading to significant volatility in the bond market.

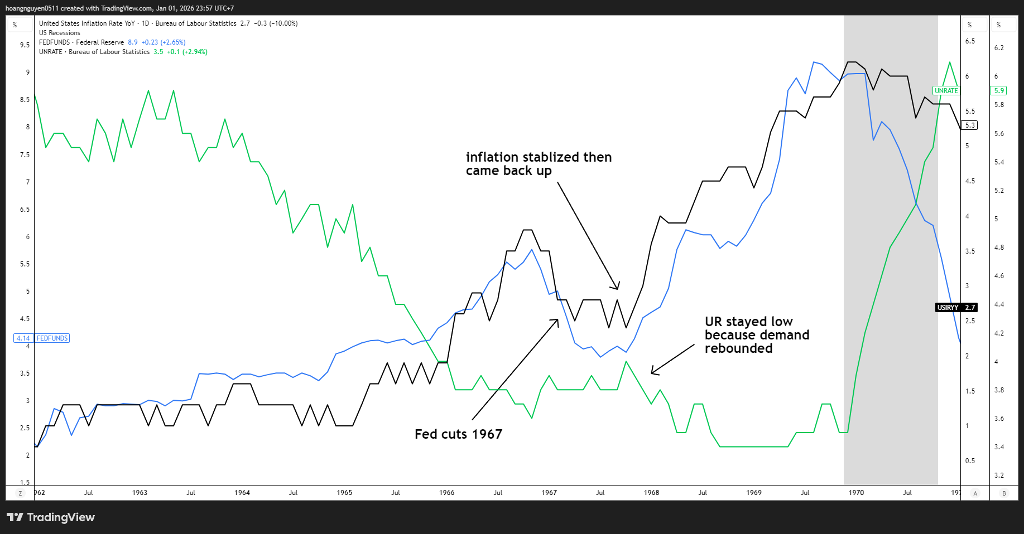

Echoes of 1966-1967

The current setup bears a striking resemblance to the late 1960s. In 1966, the Fed aggressively raised rates to cool a labor market where job openings had surged past the number of available workers – a rare phenomenon seen only a few times in history.

The tightening worked initially: vacancies declined, unemployment ticked up, and inflation stabilized. By 1967, the Fed believed they had achieved a “soft landing” and responded by slashing interest rates by a massive 200 basis points.

- The Initial Euphoria: Financial markets loved the move; yields dipped and stocks surged.

- The Policy Error: However, the labor market was still too tight. Vacancies and hiring rebounded almost instantly, supply remained constrained, and inflation began to surge.

- The Toxic End: By 1968, the Fed was forced into an even more aggressive tightening cycle, which ultimately delivered a recession by 1970.

Whether that mistake was due to political pressure or an overestimation of the labor market’s supply capacity, the risks today are nearly identical. The silver lining? If we follow the 1967–1969 timeline, the risky part of this economic consequence likely won’t hit until 2027.

The reflation trade will likely feel great for risk assets in the short term, but the underlying supply-demand imbalance suggests the “Goldilocks” consensus is on borrowed time. For now, keep riding the bull market, but stay alert – the second half of 2026 is when the debate over monetary tightening will likely turn serious.

Bottom Line

Everything right now comes down to the landing. If we nail a 1995-style soft landing, this S&P 500 bull market likely powers ahead without breaking a sweat. If the AI bubble bursts and drags us into a 2001-style recession, the floor drops out.

But if we get a 1967-style “No Landing” or a full-blown reflation trade, we are looking at a completely different environment.

You should be worried. You should prepare.

The market consensus is currently sleepwalking through a “vanilla” 2026 outlook: steady growth, drifting inflation, and central banks calmly cruising back toward neutral. To play it safe, sell-side economists have sprinkled in some mandatory warnings about “downside risks” so they don’t get blamed if things go south.

The beauty of the “K-shaped economy” theory is that it has convinced everyone that weakness at the bottom cancels out strength at the top. It’s the ultimate Goldilocks security blanket for financial markets. Whether this is a lack of imagination or just analysts “dragging Excel cells” into the future, this hyper-focus on a peaceful outlook is leaving the door wide open for a massive shock.

So, what derails the dream?

The most ironic outcome would be a U.S. recession. Why? Because it would arrive exactly when even the loudest perma-bears have stopped using the “R-word” out of pure embarrassment. Maybe the labor market is more fragile than the data suggests, or the AI bubble finally pops. But we shouldn’t trade on superstition. It’s hard to see a full recession in 2026 when the U.S. economy isn’t fundamentally broken—aside from a temporary, tariff-induced margin squeeze.

In fact, I believe the risks are skewed heavily in the opposite direction: a powerful reacceleration that shreds every forecast on the Street.

Short-term, this is a victory lap for risk assets. Stock markets live for the Reflation Trade . But with the supply side impaired – specifically a shrinking U.S. labor force – inflation risks are going to surface much faster than anyone is talking about today.

I’m not saying central banks will hike in 2026, but the conversation is going to shift in that direction very quickly. If the Fed lacks the backbone to tighten, investors will start questioning their independence.

And that is a danger zone for bonds.

Keep your eyes open. This “Agreeably Unremarkable” consensus is a trap. The data says we’re heading for a collision between a fiscal rocket ship and a supply-side wall. Ride the wave, but know where the exits are.

P.S

This is my overall base case for 2026. I will write more in depth about Europe, China, Japan, the Dollar, etc. and the trades to ride in this 2026 environment very soon. So stay tuned.

Until the next one.