Let’s talk about Kevin Warsh.

Donald Trump just nominated him to be the next Chairman of the Board of Governors of the Federal Reserve. Most people on Wall Street are breathlessly trying to figure out if he’s a hawk or a dove. I don’t think that’s the case.

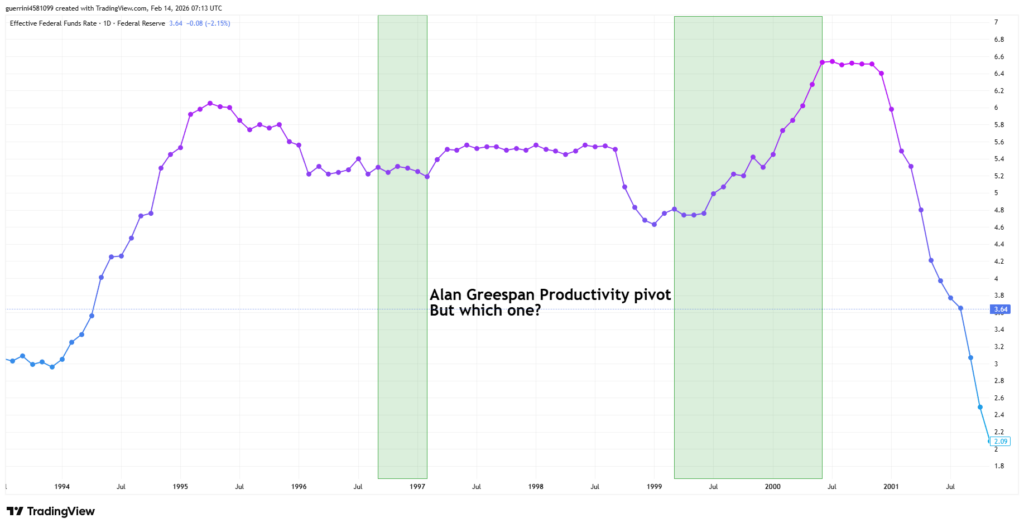

A lot of people are talking about the historical parallel here. Warsh is positioning his entire economic philosophy around the “AI Productivity Bet”. It is a direct echo of Alan Greenspan’s 1996 productivity pivot.

Back in September 1996, Greenspan entered the FOMC boardroom intent on delaying rate hikes because he believed productivity was growing faster than the official “esoteric data” showed. Janet Yellen, who was at the table, recalled that many were “completely unconvinced,” but Greenspan was “absolutely right”.

Now, Treasury Secretary Scott Bessent is out there on CNBC telling people to read Bob Woodward’s Greenspan biography to see how he “correctly let the economy run hot”. It’s a bold move.

However, the question I have for myself is which version of Alan Greenspan we should be looking at. From 1995 to late 1999, Alan Greenspan was relatively dovish compared to others in the FOMC. But Bessent, Warsh (and other doves) probably cherry pick a version of Greenspan that fits their narrative. What about the other one, the hawkish Greenspan who thought tech was inflationary?

I also find it revealing that Stanley Druckenmiller, probably the most successful speculator of his generation, now has protégés in both the Treasury and the Fed.

Reconsidering the Hawk Narrative

The branding of Warsh as a permanent hawk is a fantasy. Even his mentor, Druckenmiller, told the Financial Times, “The branding of Kevin as someone who’s always hawkish is not correct. I’ve seen him go both ways”.

Look at the evidence. Transcripts from 2008 show he was concerned about inflation just days before Lehman tilted down, but then he went “all in” on lowering rates. In 2018, he and Druckenmiller even wrote an op-ed arguing against rate hikes right before “markets fell apart”.

The evidence suggests to me that his reputation is a convenient tool. The timing of his nomination, coinciding with dollar weakness and (just a little) rising inflation expectations, feels like a tactical move. The administration is presenting him as a credible hawk precisely when they need to reassure the bond market, not because they actually want restriction.

The AI Productivity Thesis and Its Skeptics

Warsh’s core argument is that AI is “the most productivity-enhancing wave of our lifetimes — past, present and future”. He thinks this gives the Fed space to slash rates without stoking inflation.

The data tells me a different story than Warsh’s optimistic narrative. In a recent FT-Chicago Booth poll of 45 economists, roughly 60% said the impact of AI on prices and rates over the next two years would be “negligible”. Jonathan Wright, a former Fed official, was blunt: “I don’t think [the AI boom] is a disinflationary shock”.

Fed Vice-Chair Philip Jefferson even warned at Brookings that the near-term effects of AI—like massive data center construction—could actually be inflationary. Warsh needs results before the November 2026 midterms, but genuine productivity transformations take 5 to 10 years to hit the tape.

I’m on this side of the argument. I think inflation will be a problem soon before Warsh’s thesis of productivity boom kicks in.

But the AI thesis may be just a sideshow. The real constraint on whatever Warsh wants to do is the balance sheet itself — and here’s why it’s difficult to shrink it even if he genuinely wants to.

The Fed Balance Sheet

This is the heart of the matter.

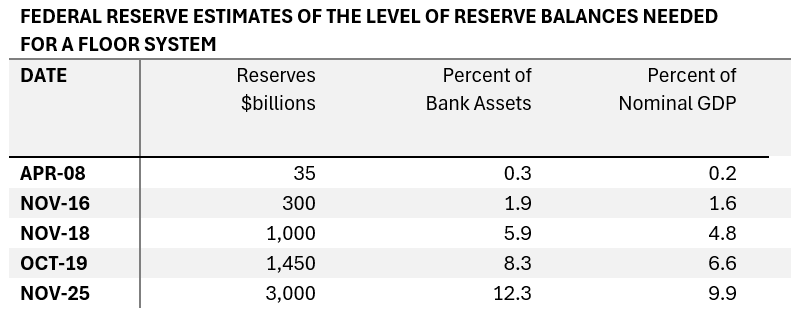

What immediately struck me about the Fed’s December 2025 decision to end quantitative tightening (QT) is not just the level at which it stopped, but the pattern it continues.

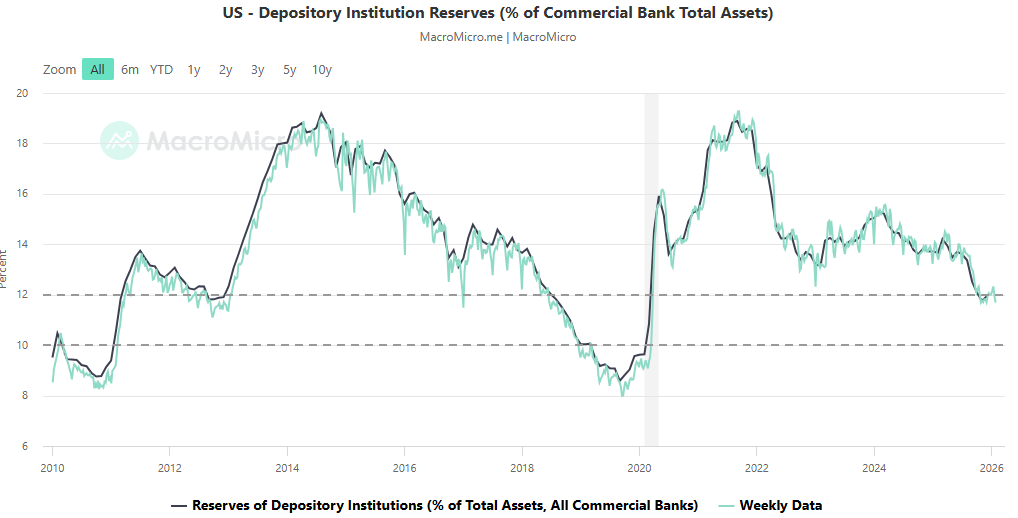

I find the pattern in “ample” reserves deeply revealing. The Fed’s estimate of what constitutes enough liquidity has moved in only one direction: upward. According to analysis by Bill Nelson, the estimates have shifted consistently over the years:

The Fed now believes it needs a $3 trillion reserve balance, which implies a minimum securities portfolio of roughly $6.5 trillion. This isn’t random variation; it’s a structural ratchet.

To understand why we are trapped here, we have to look at the combined failure of banking behavior (the addiction) and Fed operations (the plumbing).

The Liquidity Dependence Mechanism

The academics Viral V. Acharya, Rahul S. Chauhan, Raghuram Rajan, and Sascha Steffen have identified what I consider the fundamental asymmetry of our age. Their research, published in a series of papers like “Liquidity Dependence and the Waxing and Waning of Central Bank Balance Sheets” documents how QE changes bank behavior.

When the Fed expands the balance sheet, banks grow confident. They think the Fed is their personal higher power that will always backstop them. This confidence encourages them to rely on cheap, highly liquid funding sources—specifically demandable deposits (deposits that can be withdrawn immediately, like checking accounts) and credit lines. This creates “liquidity dependence”. These liabilities are a nightmare to unwind during QT, even as the reserves backing them decline. As the authors put it, “the supply of reserves creates its own demand for reserves over time”.

The Empirical Evidence

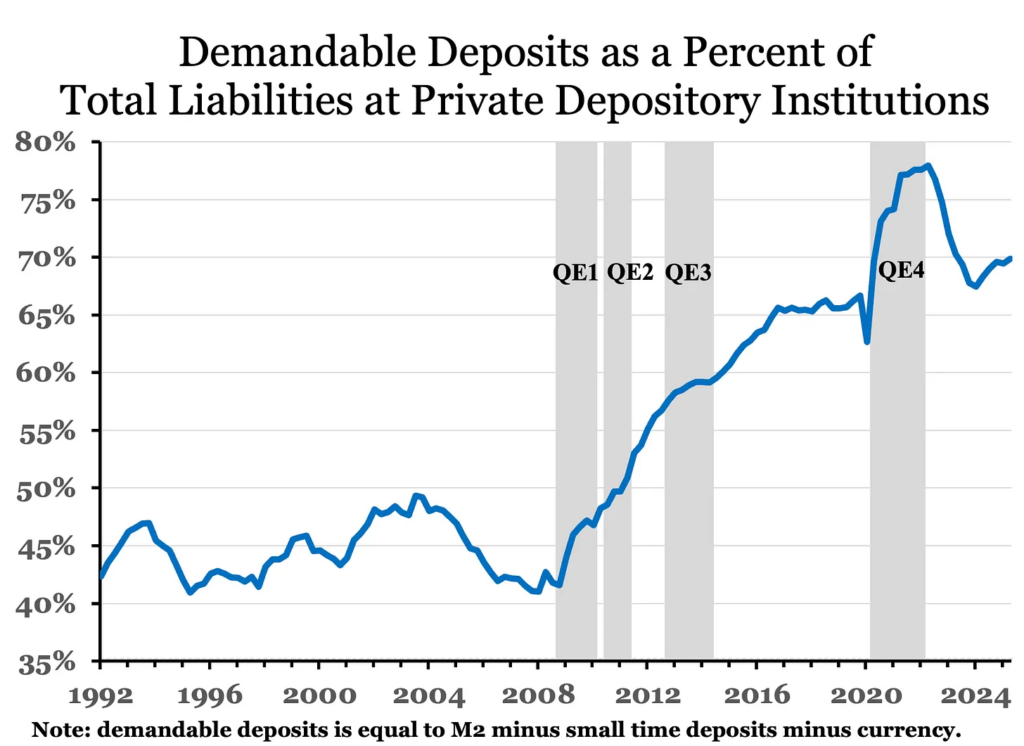

I examined the data on demandable deposits as a percent of total liabilities for private depository institutions. For decades before 2008, it averaged 40-50%. What I observe now is a steady, persistent shift toward demandable funding that accelerates during QE and simply does not reverse during QT.

This pattern contradicts what standard regulations like the LCR (Liquidity Coverage Ratio, the post-2008 rule requiring banks to hold enough liquid assets to survive a 30-day stress) would predict. Even as reserves as a percent of assets decline during QT, the demandable deposits climb. This creates a massive mismatch: growing liquid claims without proportional liquid backstops.

Using granular bank-level data, Acharya and colleagues document that this liquidity risk is becoming increasingly concentrated at small and mid-sized banks. As reserves drain from the system, liquidity migrates toward the big “systemically important” banks, leaving the whippersnappers with a growing mismatch.

The Non-Bank Channel

The problem extends beyond banks. In a 2026 paper, Darst, Kokas, Kontonikas, Peydró, and Vardoulakis document that QE-induced inflows from hedge funds and money market funds lead banks to cut back on undrawn credit lines to firms. Critically, QT does not reverse these fragile structures; it exacerbates them as reserves decline.

The core argument is that while QE adds headline liquidity (reserves on a balance sheet), it creates a chain reaction that actually makes the economy’s “contingent” liquidity more fragile.

- The Non-Bank Inflow: When the Fed does QE, it induces massive inflows of uninsured deposits from non-bank financial institutions like hedge funds, money market funds, and broker-dealers.

- The Bank’s Reaction: Banks see these volatile, uninsured deposits as a risk. To manage that risk, they start “reshaping both sides of their balance sheet”.

- The Liquidity Cut: To protect themselves, banks cut back on undrawn credit lines to firms. These credit lines are essentially the “contingent liquidity insurance” that keeps the real economy running during a shock.

- The Result: Even though there are more reserves in the system, there is actually less insurance available to firms. The “effective” liquidity—the money firms can actually count on in a pinch—goes down.

What makes this truly dangerous is that it doesn’t just go back to normal when the Fed stops. According to the authors, Quantitative Tightening (QT) does not reverse these fragile funding structures. Instead, it makes things worse: as reserves decline during QT, banks become even less willing to provide those vital liquidity backstops to the economy.

I find this conclusion striking because it turns the traditional view of QE on its head. Instead of a “flood” of liquidity that supports the economy, you end up with a system where liquidity is latently ample but practically scarce for the people who actually need it to run businesses.

The Distribution Problem, and the People Who Misread It

If Acharya explains the addiction, Andy Constan from Damped Spring explains why the intervention always fails.

The Fed currently relies on a group of internal experts led by 4 super stars to manage the plumbing of the financial system:

- Roberto Perli is the New York Fed’s balance sheet manager.

- Lorie Logan, now President of the Dallas Fed, previously held Perli’s role and spent more than a decade as a senior staff member at the New York Fed before becoming a Fed President.

- Beth Hammack, President of the Cleveland Fed, spent decades deeply involved in money markets, including serving in Goldman Sachs’ most senior role in that area.

- Alberto Musalem, President of the St. Louis Fed, worked at the New York Fed and also held market-facing positions at Tudor Investments and other private financial institutions.

This group operates on a flawed signal: they watch for spikes in the repo rate (the cost of overnight borrowing). When repo rates spike, they interpret it as a “scarcity” of reserves. Their solution is reflexive: stop QT and flood the system with liquidity.

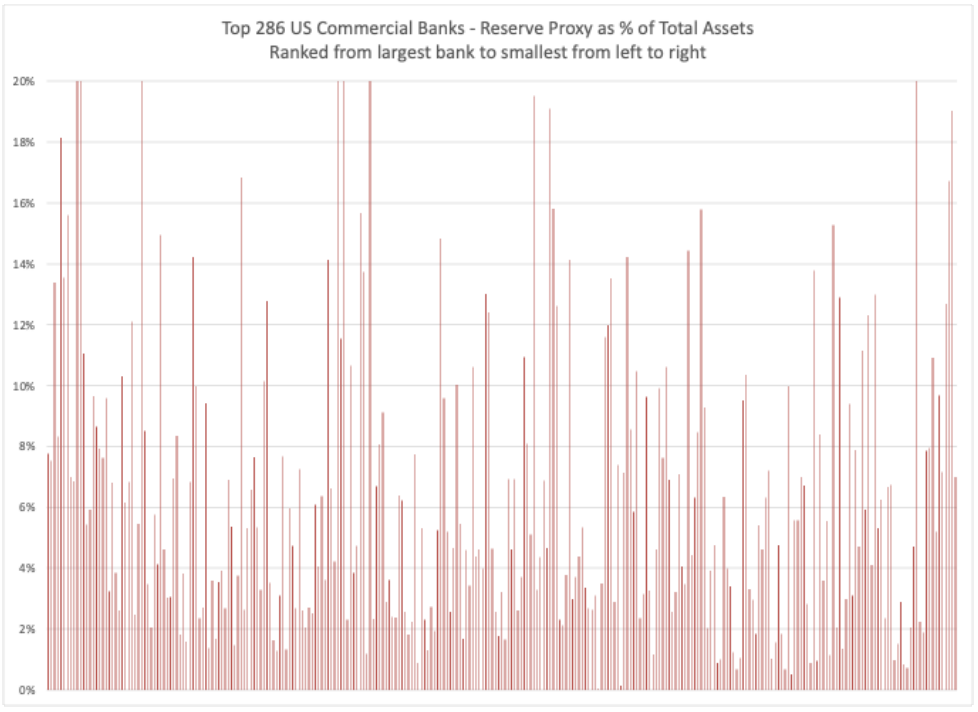

However, the problem is rarely a total lack of cash. The problem from Andy Constan’s view is distribution.

- The Hoarders: The largest 50 banks are currently sitting on massive piles of excess reserves, effectively hoarding liquidity.

- The Starved: Meanwhile, hundreds of smaller and mid-sized banks are running on fumes, creating the illusion of a systemic shortage.

Because the big banks hoard cash (partly due to regulatory incentives), the reserves don’t flow to where they are needed. The Fed misreads this plumbing failure as a solvency crisis, causing them to abandon QT prematurely.

Historical Stress Episodes

Through this lens, our recent financial crises look different. They aren’t random accidents; they are structural failures of this mechanism.

- September 2019: Standard narratives blame corporate tax payments for draining cash. The reality was that the system was already overloaded with “potential liquidity claims” (Acharya). When the Treasury General Account (TGA) refilled, it drained reserves from the system. Because the big banks hoarded what was left (Damped Spring), the repo market snapped.

- March 2020: This was the ultimate “dash for cash.” Corporations rushed to draw down the credit lines that banks had happily written during the good times. The banks, facing a sudden realization of their own liquidity dependence, stopped lending, forcing the Fed to intervene on a massive scale.

- March 2023 (Silicon Valley Bank): SVB was the extreme example of the “Liquidity Dependence” thesis. It gorged on uninsured deposits during QE. When QT exposed the mismatch, the liquidity didn’t flow from the big banks to save them; it stayed trapped at the top.

Why Reduction Keeps Failing

The pattern is clear: each QE episode encourages the expansion of runnable claims that get embedded in bank business models. When QT begins, reserves decline but the claims don’t. The mismatch widens until a repo spike or a regional bank failure forces the Fed to expand again at a higher level than before. The ratchet clicks upward.

Warsh inherits a balance sheet at $6.6 trillion. He says he wants to return to pre-2008 levels—under $1 trillion. That’s a $5.5 trillion reduction. Given that the 2019 crisis happened when reserves were still at $1.5 trillion, I find it impossible to envision how we get to $1 trillion without encountering severe, repeated liquidity stress.

The Riksbank Solution: A Potential Path Forward?

So, how do we fix it? We can’t just keep supplying more reserves.

The Swedish central bank, the Riksbank, might have the answer. They operate a narrow corridor around their policy rate:

- Term Deposits: Offered at the targeted policy rate.

- Overnight Deposits: Earn 10 basis points below the policy rate.

- Overnight Lending: Available at 10 basis points above the policy rate.

This creates a demand-driven system. Banks choose whether to hold overnight reserves or term deposits. They are incentivized to minimize idle reserves because term deposits pay more.

If the Fed elevated its existing Term Deposit Facility (TDF)—which has existed since 2010 but is mostly just sitting there gathering dust—it could fundamentally change the game. By introducing maturity into the Fed’s liabilities, banks would stop treating reserves as a costless backstop for short-term gambling.

Crucially, balance-sheet normalization would become the “natural, automatic default”. When QE ends, the term deposits would just roll off at maturity unless they were renewed. No more Repo spikes.

Ending liquidity dependence doesn’t mean we have to stop doing QE forever. It just means we need to stop making mistakes on how we price it. Discipline when nothing is happening. Elasticity when something is.

It’s an intellectually compelling idea. The question is whether Warsh has the stomach to manage the transition without triggering the very stress he wants to prevent.

The Policy Mix: All Roads Lead to Accommodation

When I think about the Trump administration’s policies, I see that virtually every lever is being pulled in a stimulative direction.:

- Fiscal Policy: Depends on how we calculate but I think we can assume it’s roughly 0.5%-1% addition over 2026, front-loaded to Q1.

- Prudential Supervision: Reducing headcount by 30% sends an unmistakable signal to the banks.

- Tax Policy: Depreciation allowances made permanent.

- Deregulation: The “Unleashing Prosperity” initiative and an Investment Accelerator to fast-track projects.

- FX Policy: Recent intervention to manage a lower dollar.

Every stimulative policy lever is active. The sole exception is tariffs. This tells me the “reshoring” agenda is the core, and its negative effects must be offset by aggressive stimulus everywhere else. There were signs the dollar was weakening too fast; you don’t boil frogs if you turn the heat up too high. Warsh’s nomination is a mechanism to rein in the idea that the dollar is a one-way bet—it’s tactical cover. Probably.

Conclusion

Trump wants rates at 1%. Warsh (probably) wants a balance sheet close to 2008-level ($1 trillion). And structural reality—the liquidity dependence ratchet—says you can’t have either without a financial crisis.

Current FOMC forecasts project rates staying above 3.25% through 2026. That is nowhere near the 1% Trump wants. Warsh’s desire to reduce the Fed’s footprint is in direct, irreconcilable conflict with the behavior of the banking system. The shift toward demandable liabilities isn’t a policy choice; it’s an addiction.

Here’s my prediction: regardless of Warsh’s stated philosophy, monetary policy will remain surprisingly accommodative. The balance sheet will not shrink meaningfully. If they try, financial stress will force a re-expansion at an even higher level. The market’s addiction to reserves is more powerful than any individual Fed Chair’s preferences. Warsh represents the exception that proves the Trump rule: the hawkish branding provides reassurance, while the actual trajectory continues toward accommodation.